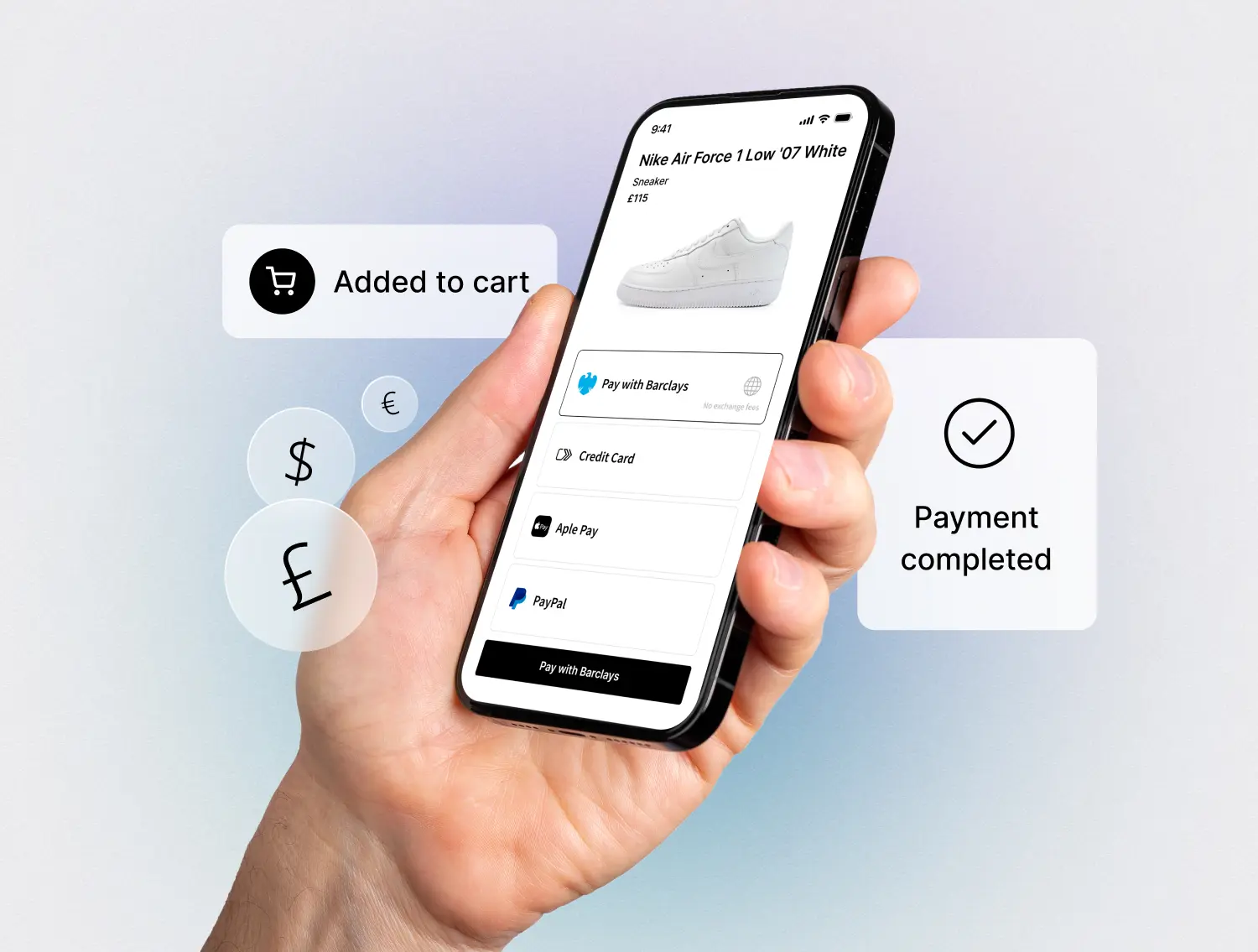

October 14, 2025: Quidkey, a leading fintech in account-to-account (A2A) payments, has chosen TransferMate, the world's leading provider of embedded B2B payments infrastructure as a service (IaaS) to power global A2A payments for e-commerce merchants. The collaboration unlocks a faster, cheaper alternative to traditional card payments for merchants operating across the UK, EU, and US.

Through this embedded solution, both companies will harness Open Banking technology to replace costly card rails with a faster, more efficient model of payments. TransferMate's global network of payment licenses and banking integrations will allow Quidkey to extend its cross-border payments capabilities to merchants worldwide.

Founded in early 2023, Quidkey has quickly established itself as a trusted provider of next-generation A2A payments. Leveraging AI-powered bank prediction, instant settlement, and a streamlined user experience, Quidkey is redefining how global businesses collect payments.

"Partnering with TransferMate gives our merchants a truly global reach. Their infrastructure and regulatory footprint mean we can offer seamless, low-cost cross-border payments without compromise," said Rob Zeko, Co-Founder & CEO of Quidkey.

For merchants, the solution means a reduced dependency on expensive credit card processing, faster settlement cycles, and the ability to expand into new regions with confidence. For consumers, it means a smoother, faster checkout experience without the friction of traditional payment methods.

"We're excited to power Quidkey's global expansion. Together, we're giving merchants a modern payment rail that reduces costs and accelerates cash flow — essential ingredients for growth in today's e-commerce landscape," said Gary Conroy, CEO of TransferMate.

The Open Banking market is forecast to grow from $35 billion in 2025 to $94 billion by 2029 and $180 billion by 2032. With Quidkey's next-gen payments innovation and TransferMate's largest fintech payments network, the partnership is poised to capture significant share of this rapidly expanding market.

About TransferMate

TransferMate is a leading provider of embedded B2B payments technology, helping companies, software providers & financial institutions to streamline their global receivables, payments, & local account management processes. TransferMate's innovative technology platform simplifies business-to-business and consumer payments for clients in more than 200 countries.

About Quidkey

Quidkey is on a mission to become the merchant-facing clearing abstraction layer, enabling borderless A2A checkouts that drive personalisation, boost conversion, enhance security, and build on existing customer-bank trust.

Our approach creates value across the ecosystem:

- Consumers enjoy frictionless, bank-authenticated payments with protections.

- Merchants save on processing costs, increase conversions, and reduce fraud/chargebacks.

- Banks strengthen customer primacy and democratise access to their products at checkout.