Open Banking Payments in the UK

Accept Open Banking payments in the UK with instant settlement, no chargebacks, and lower fees. Complete guide for UK merchants.

4 min read·Read article→

Pay by Bank lets customers pay directly from their bank. Lower fees, instant settlement, no chargebacks. Learn how it works globally.

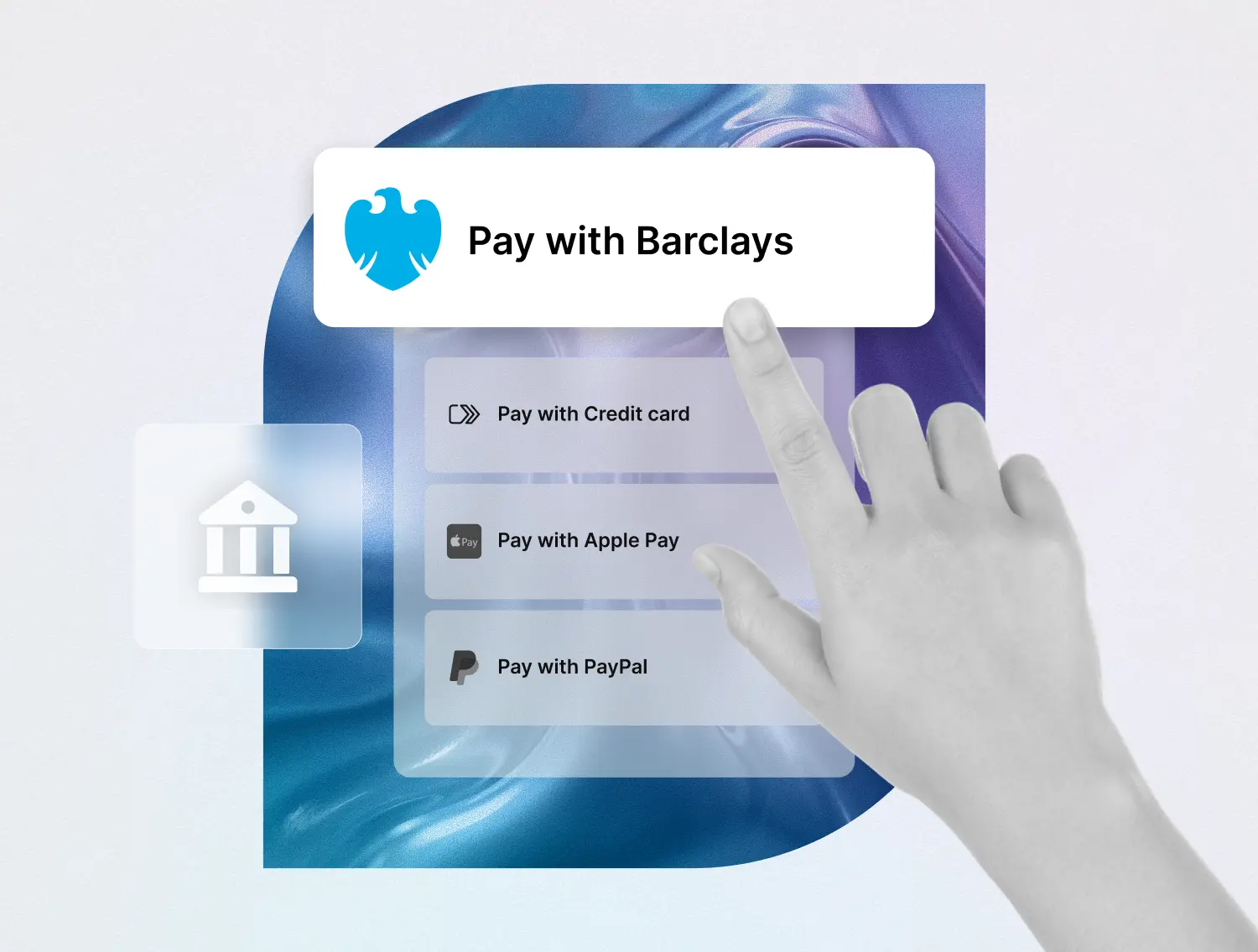

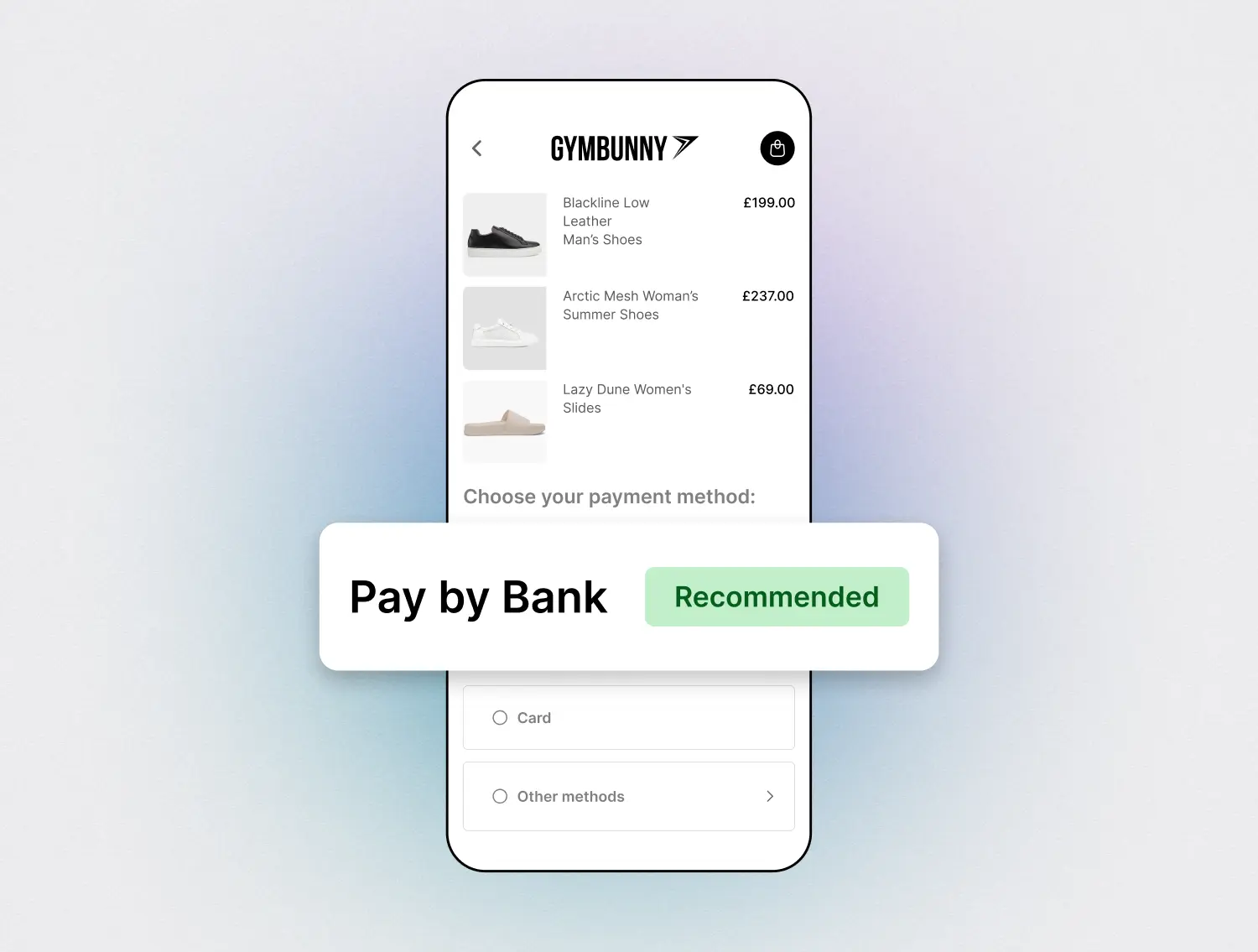

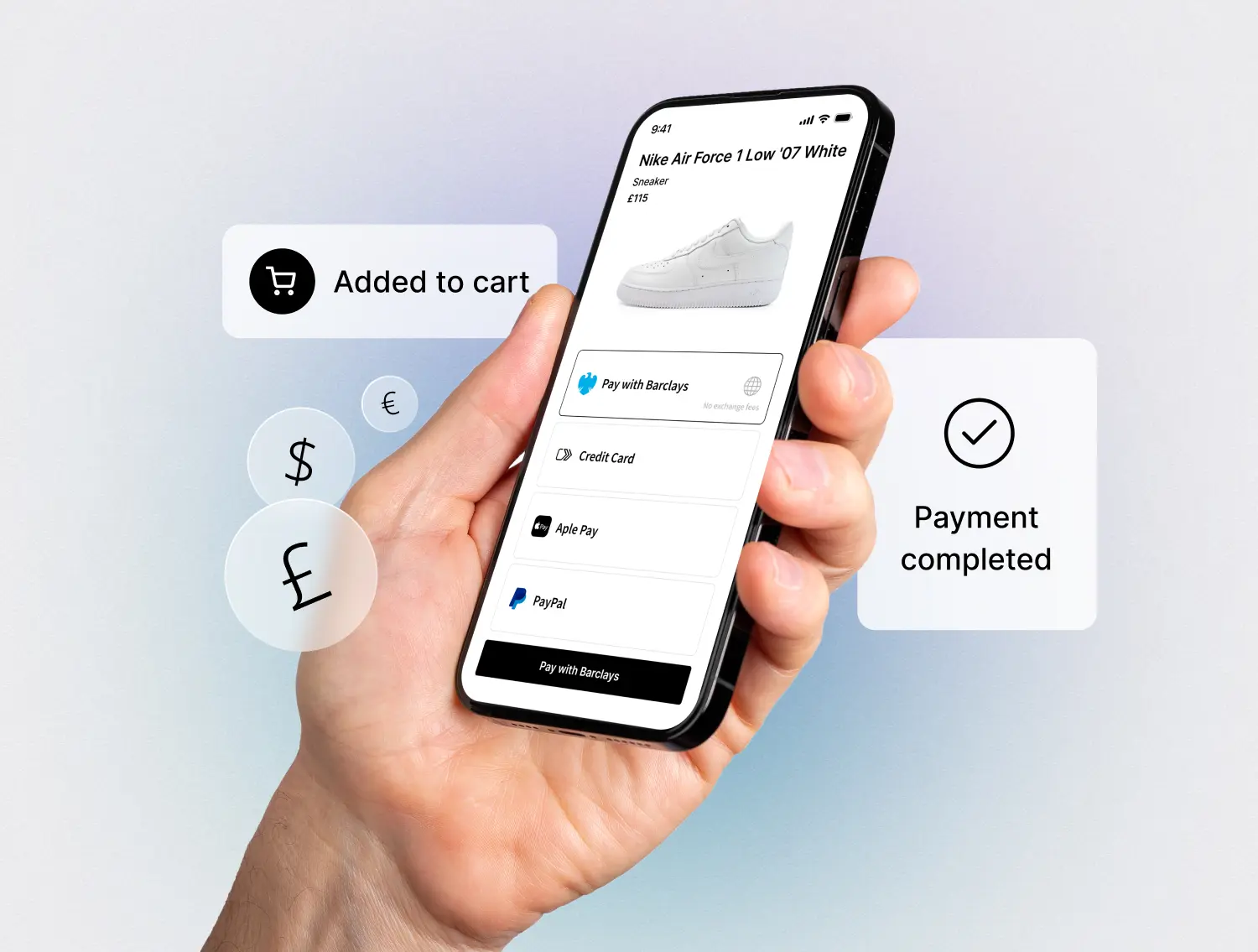

Pay by Bank is a fast and secure way for customers to pay directly from their bank account at checkout. Instead of entering card details, the customer selects their bank, approves the payment in their banking app, and the funds are transferred instantly. No card networks. No intermediaries. Just a direct, secure payment.

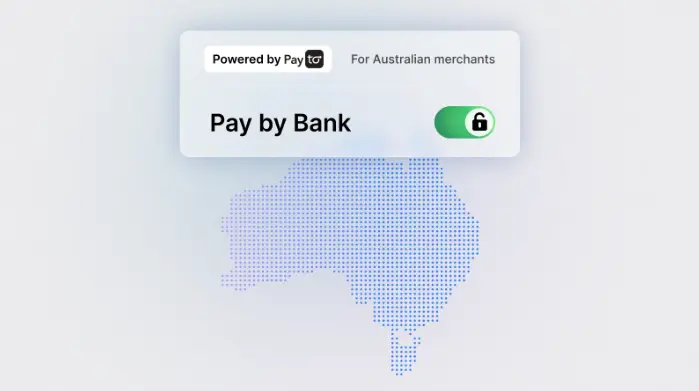

In the United Kingdom, Pay by Bank is powered by Open Banking and the Faster Payments network. Across Europe, it runs on SEPA/Instant SEPA, and similar systems are now emerging worldwide, including PIX in Brazil, UPI in India, and FedNow in the United States.

No card numbers. No intermediaries. No risk of stolen details.

For businesses, Pay by Bank is not just another payment option. It is a way to solve some of the biggest challenges in online commerce:

While the United Kingdom has led adoption, Pay by Bank is expanding rapidly across global markets:

Merchants everywhere are embracing Pay by Bank for its lower costs and stronger security. The challenge is that most of these systems are designed for domestic payments, and using them across borders remains fragmented and expensive.

Pay by Bank is powerful but fragmented. Each country runs its own rail and most providers only connect to a limited set of them. For merchants, this creates unnecessary complexity.

Quidkey solves this with one integration and global reach. Our platform connects to multiple providers and networks across markets, and Quidkey orchestrates the best route for every transaction.

Here is how Quidkey makes Pay by Bank work for merchants:

Quidkey is available to merchants in more than 90 jurisdictions, enabling sales into the UK, EU, US, and Australia.

Pay by Bank is more than a buzzword. It is a smarter, safer, and cheaper way for merchants to get paid. The model is already live in the United Kingdom and is rapidly expanding worldwide.

With Quidkey, you can enable Pay by Bank through a single integration, reduce your costs, eliminate fraud and chargebacks, and unlock a global payment solution built for merchants.

Accept Open Banking payments in the UK with instant settlement, no chargebacks, and lower fees. Complete guide for UK merchants.

A2A payments offer 70% lower fees than cards, instant settlement, and zero chargebacks. Learn why UK merchants are switching.

PayTo is Australia's real-time bank payment system. Learn how it works, the fee savings, how it handles fraud, and how to add Pay by Bank to your store.