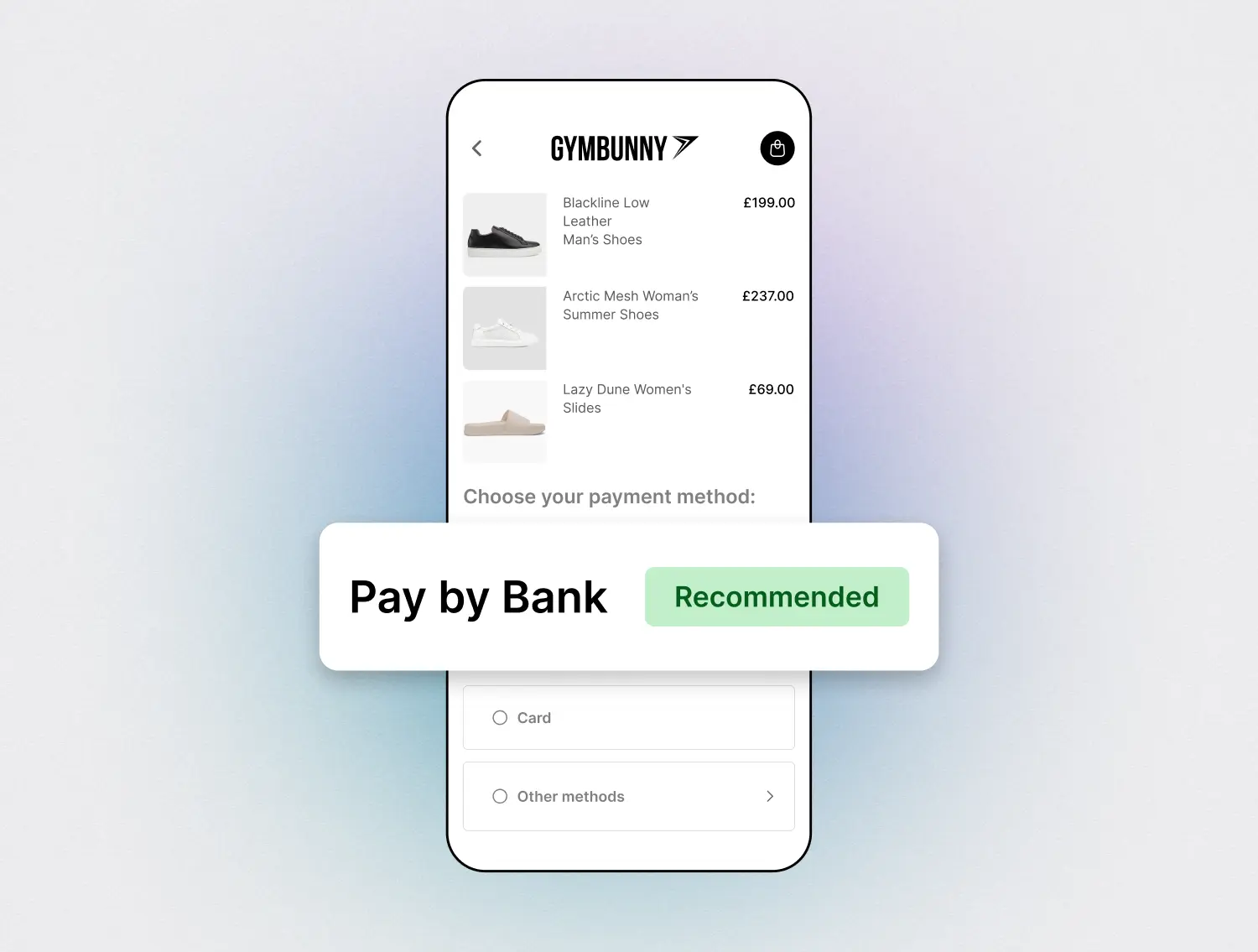

Pay by Bank: The Future of Payments

Pay by Bank lets customers pay directly from their bank. Lower fees, instant settlement, no chargebacks. Learn how it works globally.

4 min read·Read article→

Accept Open Banking payments in the UK with instant settlement, no chargebacks, and lower fees. Complete guide for UK merchants.

Open banking is a regulatory and technological framework that allows consumers and businesses in the United Kingdom (UK) and European Union (EU) to securely connect their bank accounts and share their financial data with authorised third-party providers. These providers can:

To ensure improved consumer protection and lower fraud rates, the open banking framework also requires heightened security standards to manage consumer authentication and protect consumer data.

To make this secure and scalable, UK regulators required all major banks to implement standardised APIs. These APIs allow licensed developers to build services on top of bank infrastructure without compromising security or privacy.

Open banking started as a regulatory initiative under the European PSD2 directive, with the goal of increasing competition, transparency, and innovation in financial services. In the UK, it was driven forward by the Competition and Markets Authority (CMA).

Today, open banking is no longer experimental. In the UK alone, over 15 million users rely on open banking services every month, and the infrastructure is subject to oversight and control from the Financial Conduct Authority (FCA).

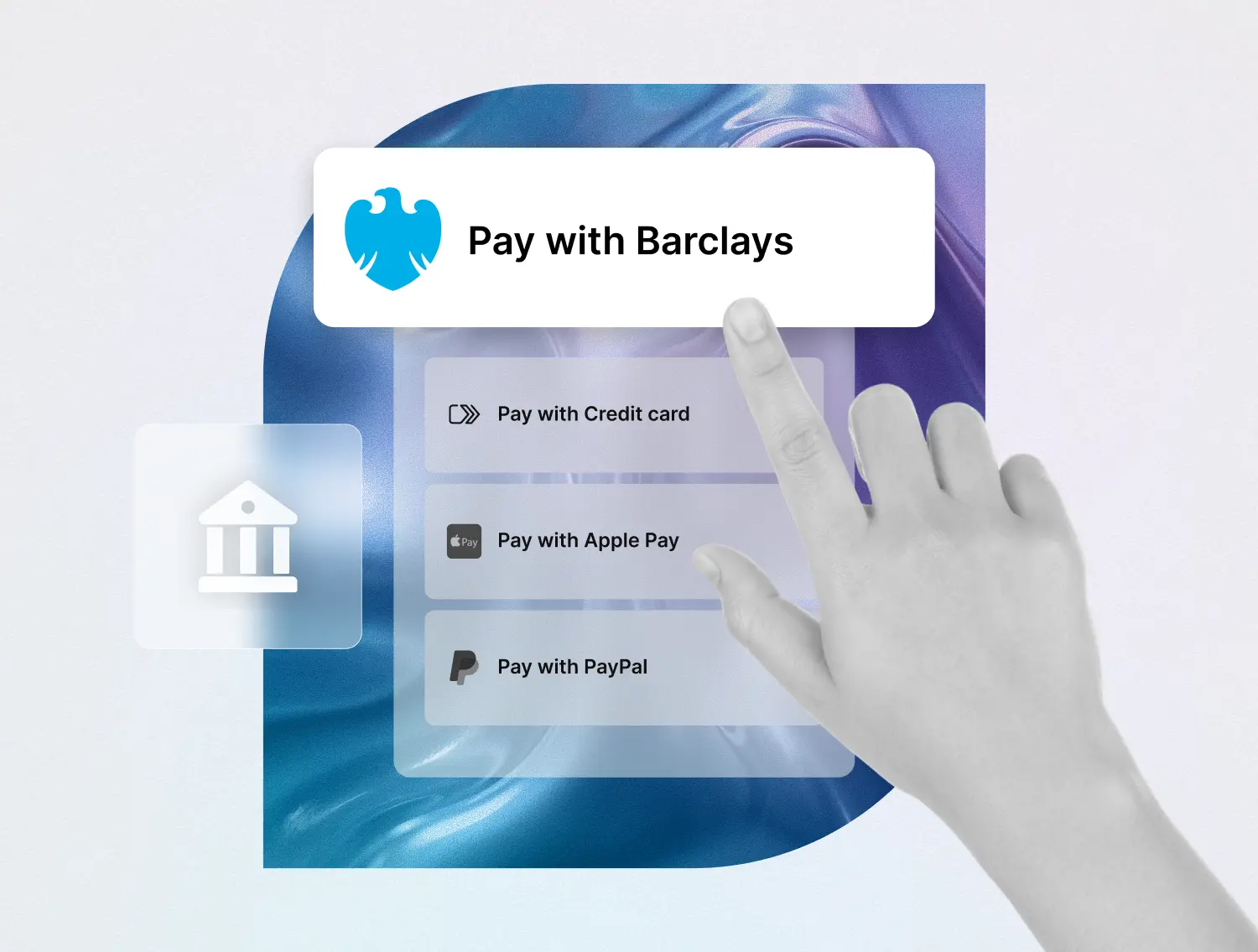

Open banking is already powering a range of useful services across the UK and the EU. Here are a few common examples:

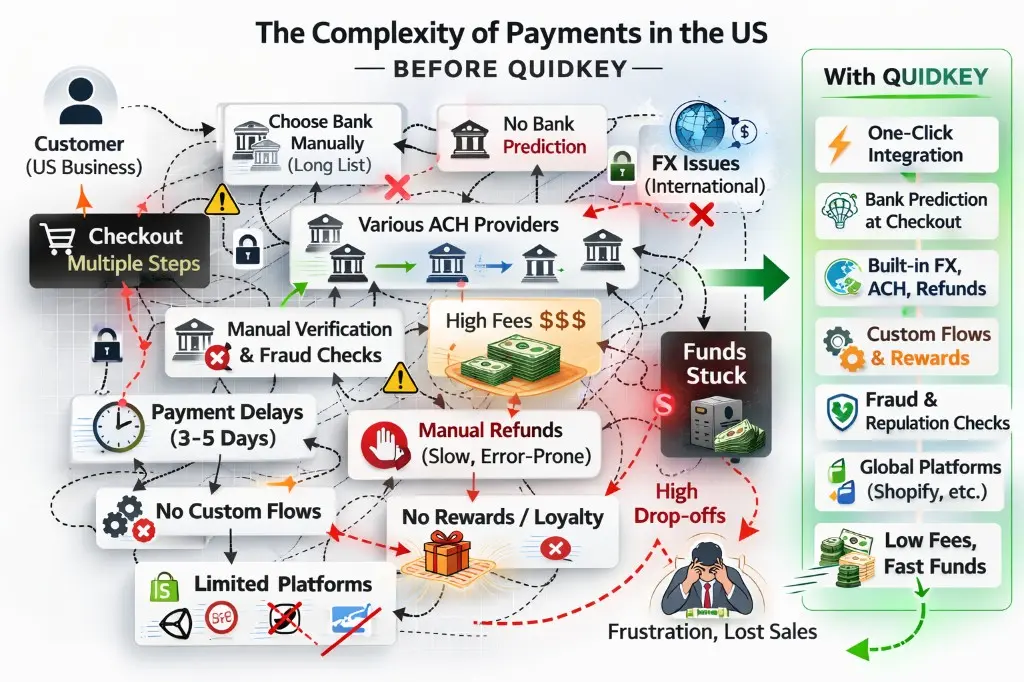

If you are a UK business looking to accept open banking payments, the process can be time consuming and complex. Here's what most businesses face:

At Quidkey, we handle the complexity so you can be free to focus on your business. Our platform connects to multiple third party providers across different markets and automatically selects the best path for each transaction.

Quidkey simplifies payments so you can focus on growing your business. Accept payments across borders, support multiple currencies, and go live in minutes.

Open banking provides the rails. Quidkey makes them usable.

While providers like Tink, TrueLayer, and Token offer secure access to bank accounts, they stop short of delivering the full checkout experience. Quidkey fills that gap by combining real time orchestration, bank prediction, cross-border support, and merchant-ready integrations.

Quidkey is not just another payment provider. It's open banking actually done right.

Instant payouts. No fraud. No chargebacks. Lower fees. Seamless integration.

Go live in minutes and take control of how your business gets paid.

Pay by Bank lets customers pay directly from their bank. Lower fees, instant settlement, no chargebacks. Learn how it works globally.

Learn how open finance in the US works, how it differs from EU/UK open banking, and how Quidkey solves fragmentation for global A2A payments.